Today, Puzzle becomes ZKPuzzle.

Same company, same team, four-year arc — Nucleo → Puzzle → ZKPuzzle — building the consumer-facing surface for triple-entry bookkeeping. AI is taking jobs — and triple-entry is what gives the people affected a real stake in the upside instead of being shut out of it.

Below: why now, why we started, why us to ship it, the bet.

Why now.

The question on everyone’s mind in 2026 is some version of: how will we adjust to the AI upheaval?

The problem: risk of economic and societal collapse.

It’s not a future-tense question anymore. In February 2026, Block cut about 40% of its workforce and explicitly cited AI as the reason. In April, Snap cut 16% of its workforce — and the stock went up. The market is rewarding labor displacement, not punishing it. The way the largest AI companies are now valued is consistent with a much harder thesis — that human labor itself is the addressable market, with intelligence sold as a metered utility — captured most clearly in Citrini Research’s 2028 GIC piece.

The public reaction is, predictably, hatred. The New York Times asked “Why do Americans hate AI?” in January 2026. Recent polling shows Americans hate AI more than they hate ICE. This isn’t a fear of futuristic robots. It’s a present-tense civic posture against the deployments people are already living through.

This pattern has resolved before, and the resolution wasn’t pretty. When the cotton gin made cotton the American economy’s dominant export, the wealth flowed to plantation owners and Northern textile mills — not to the enslaved people whose labor created it. The economic structure became profitable enough to entrench, and the resolution required the Civil War. The second industrial revolution played out a smaller-scale version of the same dynamic — a generation of labor violence (Ludlow, Pullman, Homestead) before the New Deal rebalanced who held the upside.

The 2026 moment is structurally analogous, and the canaries are already singing. Luigi Mangione — the man accused of assassinating UnitedHealthcare’s CEO — has fan clubs and a growing cultural following. Sam Altman’s home was targeted in two separate attacks in April 2026 alone. The resolution doesn’t have to involve violence. But it has to give the people affected a real stake in the upside.

Peter Thiel has put it crisply: people without a stake in a system tend to turn against it. The hatred isn’t irrational — it’s the predictable response of a population economically excluded from the upside of a transition reshaping its labor market. The current AI economy has a cap-table structure that excludes almost everyone affected by it.

“You’ll own nothing, be happy” was supposed to be a warning. By 2026 it describes where labor markets are heading by default.

The OpenAI engineers, the Anthropic researchers, the Cursor and Perplexity teams whose work is causing the labor compression — they aren’t revolting against their own companies. The reason is structural, not moral: their offer letters include salary and equity. They have a stake in the upside of the very transition they’re driving. Almost everyone affected by AI labor compression is on the other side of that line — without the equity, tokens, or participation rights that keep the engineers from turning against their own work.

Two paths from here, if nothing fundamental changes:

Economic catastrophe. Cities with empty skyscrapers as teams downsize on AI productivity gains, fending off a warring army of entrepreneurial individuals more capable than ever. Private credit marks down 90%+ as an industry. Private equity 90%+. Commercial real estate 90%+. Everyone blocked out of AI-related tokens or equity. No stake in the upside.

Societal catastrophe. Underinvestment in energy and compute, or overregulation, results in heavily metered intelligence — affordable only by AI labs and the existing large businesses paying them. Individuals lose the ability to compete. Profits continue flowing to the top. The K-shaped economy accelerates into a permanent underclass. Class violence escalates.

The solution: triple-entry bookkeeping.

The mechanism that is already protecting one specific cohort has a name in accounting theory: triple-entry bookkeeping. Every entry in an AI engineer’s offer letter is a debit, a credit, and a token — the equity grant. The token is what gives them a stake in the upside. The reason it has only ever worked at scale for one specific lane of organizations (VC-backed software companies — MIT’s Energy Initiative documented the structural mismatch with capital-intensive sectors in their 2016 analysis of cleantech VC) isn’t moral or ideological. It’s that the legal, financial, and privacy primitives required to extend the mechanism to every kind of organization didn’t exist at production quality. For the first time in fifty years, they do.

Different flavors of triple-entry have existed for decades across other industries — commissions, partnerships, dividends, points programs, carry, affiliate revenue shares. But each version has been industry-limited or scale-limited. None has been able to reach global consumer scale (1B+ users, every category of organization). That’s what’s now changing — and not by accident. Several industry currents have finally converged to make it possible: stablecoin standards crossing into production-grade settlement rails, data-availability layers maturing into infrastructure that can support consumer-scale throughput, regulatory clarity emerging in the largest jurisdictions, and crypto economics stabilizing into something institutional capital can actually underwrite.

It’s also what we’ve spent the last four years building the technology and product suite to ship at scale. ZKPuzzle is what we’ve built it into.

Why ZKPuzzle?

ZKPuzzle is the company Matt and his co-founder Luke started in 2022 to bring triple-entry bookkeeping to global consumer scale. The brand has changed three times along the way — Nucleo first, then Puzzle, now ZKPuzzle — as the product surfaces evolved. The mission hasn’t.

Why we started.

The why is partly biographical. Matt’s college years put him in technical proximity to two of the largest computational shifts of the last two decades simultaneously — the deep-learning wave (working on neural networks in industry research in 2016) and the crypto/blockchain revolution (took Georgia Tech’s first blockchain course in 2018). He was in the blockchain-not-crypto crowd — enterprise-focused, broadly dismissive of consumer crypto.

The lightbulb moment.

That changed in late 2021 with ConstitutionDAO. Forty-seven million dollars of internet money pooled in days to bid on a copy of the United States Constitution at Sotheby’s. The bid lost. Ken Griffin outbid them at $43.2M. The DAO’s effective ceiling was visible on-chain to anyone watching — a privacy gap that arguably cost them the auction. The part that mattered most happened after the bid failed. Every donor had received a PEOPLE token; the team made the tokens tradeable; and the token kept going. It hit ~$400M market cap in early 2022, then ~$600M in 2024 driven by a different cultural community that found it years later. Four years after the auction loss, PEOPLE still trades with 19,000+ holders. That was the lightbulb. Triple-entry bookkeeping wasn’t theoretical anymore — it was working in production, at scale, in public.

What I already saw.

The lightbulb clicked because I’d already watched the structural problem destroy people I knew. The DOE researcher whose commercializable breakthrough got partnered out to industry on terms that paid her institution a flat licensing fee while the company that productized it captured millions in equity she ’d never see. The professional services consultant who built a new line of business — onboarded the early customers, designed the methodology, hired the team — then watched the revenue accrue to firms and partners who hadn’t built any of it. The Bird hardware engineer whose company got vultured between capital markets demanding faster growth and city governments wanting scooters off the sidewalk, watching her equity get wiped out alongside the work. Same pattern every time: value created in one place, captured in another, because the people who created it held no real stake in the upside they were producing.

The most extreme version of that pattern was scaled to a region, and it was his hometown. Lafayette, Louisiana — one of the offshore oil industry’s regional capitals after New Orleans. After BP Macondo and the post-2014 shale glut, the legislature cut higher-education funding sixteen times in nine years. Tuition at the University of Louisiana at Lafayette rose 140%. The share of the state’s population economically tied to government payroll or major transfer programs roughly doubled — from about a third in the mid-2010s to about half today. The downtown oil center emptied out. The firms that had captured the upside during the boom years had no stake in the city’s resilience after the bust. They relocated. The residents who had helped them grow were left with no ownership claim on what came next, and no economic mechanism to soften the blow. None of it was malicious. All of it was structural.

For fifty years, that structural pattern had no technical fix — only political ones that arrived late, at high cost (the Civil War, the New Deal, decades of labor violence in between). A technical fix finally exists. What follows is what changed.

The four-piece kit.

The mechanism that extends triple-entry bookkeeping from one specific lane (VC-backed software) to every kind of organization isn’t a single innovation. It’s the convergence of four primitives that all needed to reach production quality at the same time.

Smart contracts (legal-and-contracting friction). For most of legal history, multi-party arrangements with shared upside have required lawyers in the loop on every change. Joint ventures, partnerships with carry, profit-sharing agreements — the friction of writing, executing, and amending the contracts has kept these structures expensive and bespoke. Smart contracts express the same arrangements in code that runs deterministically without intermediaries. The contract is the execution. That doesn’t mean lawyers go away; it means the legal-engineering loop closes from quarters to milliseconds for any participant.

Stablecoins (money-movement friction). For triple-entry to work, the cash leg of any transaction has to settle predictably and quickly. Until 2023 or so, that meant either rails like ACH and SWIFT (slow, expensive, intermediated) or volatile crypto-native assets (impossible to budget around). Stablecoins solve the volatility problem while inheriting crypto-rail speed. Settlement infrastructure has matured enormously between 2022 and 2026. Stablecoins now clear a substantial fraction of the world’s digital payments, denominated reliably in USD-equivalent units. In practice: a Shopify shop in 2026 can settle giveaways, payouts, and revenue shares in seconds at near-zero friction, with denomination guarantees that didn’t exist five years ago.

Crypto markets (liquid-token-redemption friction). A token is only useful if it has discoverable value — and discoverable value requires a full ecosystem of market participants, not a few enthusiasts trading among themselves. The early crypto era had thousands of tokens with no markets, no liquidity, no institutional presence. That’s no longer true. The participant base is now deep across every tier: zealous believers, retail individuals and active traders, decentralized exchanges, institutional market makers (Jump, Jane Street, Citadel Securities, Wintermute), spot-asset ETFs across the major crypto assets, institutional investment managers (BlackRock, Fidelity, sovereign allocators), and a growing roster of public companies holding crypto on treasury. Most of the institutional half of that list — ETFs, asset-manager allocations, public-company treasury adoption — has matured in the last year alone. The result is a market where most legitimate tokens have actual price discovery, and the path from “I hold a token” to “I hold real-economy value” is short and well-understood. That’s the difference between an IOU and a tradeable asset.

Zero-knowledge proofs (privacy, scalability, and verifiability friction). The cryptographic layer that does three jobs at once: lets organizations and counterparties engage on the rails above without exposing their books to the world (privacy); compresses chain throughput enough to support consumer-scale usage (scalability); and produces mathematically-checkable guarantees rather than trust-based ones (verifiability). Until ZK reached production quality across all three dimensions in 2024–2025, this was the binding constraint. A multi-party arrangement on a fully public chain leaks the cap table, the customer list, and the financial state — which is why no serious organization would adopt it. ZK lets organizations participate in the same rails the AI engineers’ equity grants run on, without exposing the things they couldn’t afford to expose.

Each track, separately, was insufficient. Together — and only together — they enable triple-entry at scale for every kind of organization.

ZKPuzzle: the kit running today.

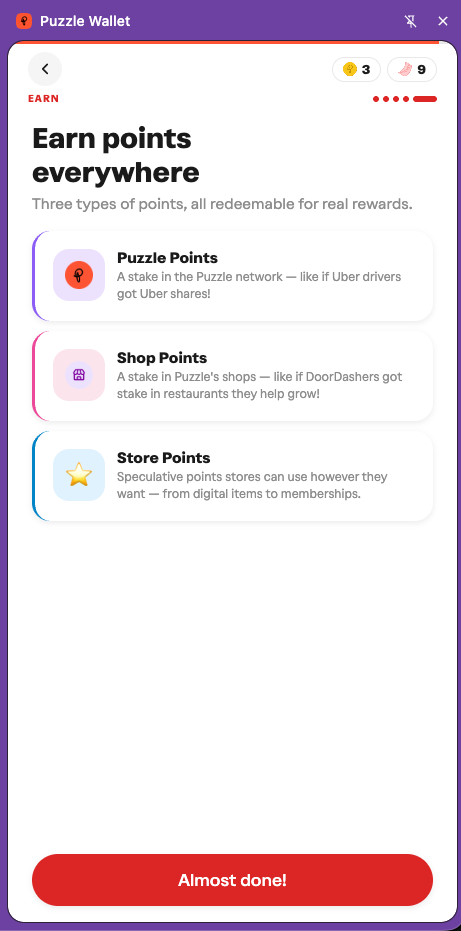

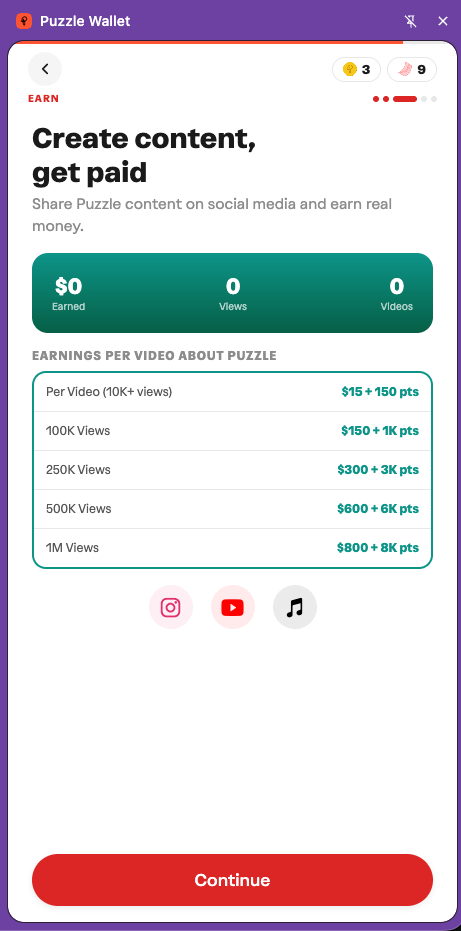

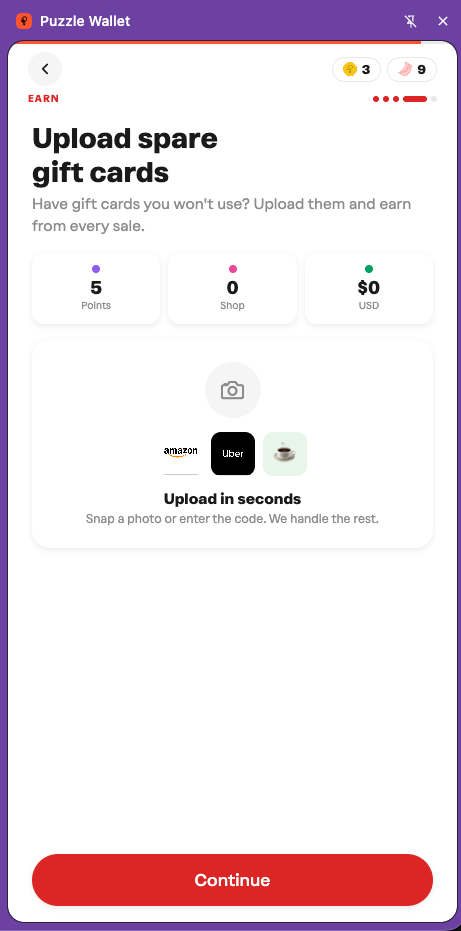

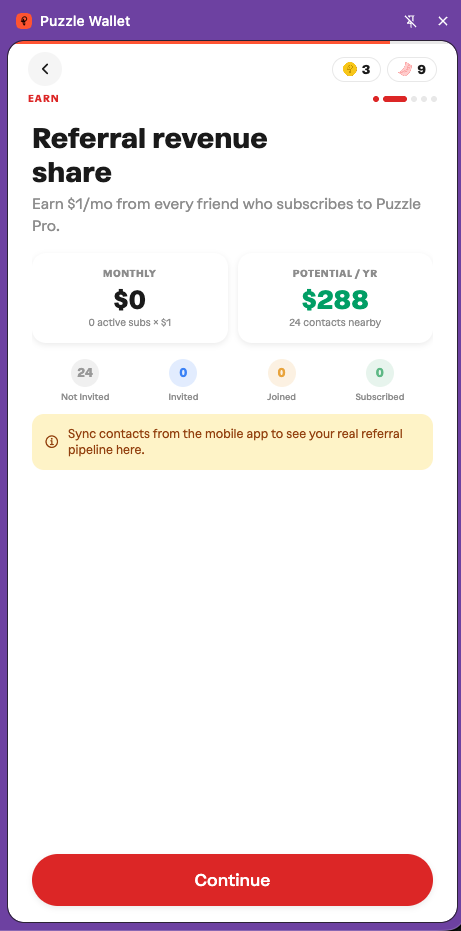

Theory aside — here’s the four-piece kit running in production today. The screens below showcase triple-entry bookkeeping at consumer scale: every user action that grows the ZKPuzzle network, the shops ecosystem, or an individual store earns a stake — privacy, scalability, and verifiability all enabled by ZK proofs.

Why us to ship this at scale?

What follows is the four-year track record — partly deliberate execution toward the thesis, partly recognized accident along the way. We were strategic about the destination: bring more organizations onchain, make triple-entry bookkeeping normal, build consumer surfaces that turn the new primitives into products people use. We were less strategic about the route. The strategic part has stayed constant. The route is what produced the specific shape of the company we are today.

The four-year track record.

Nucleo era.

2022 — Nucleo. We shipped privacy crypto infrastructure for organizations. The $4M seed round (Nov 2022) was led by Bain Capital Crypto and 6th Man Ventures, with Aleo, Aztec, and Espresso Systems as strategic co-investors. By early 2023, 20+ onchain organizations were using Nucleo as a private multisig — MakerDAO among them — and the toolkit ran $1M+ in TVL on Aztec. Working with those customers exposed the next-order problems they actually needed solved — distribution, multichain wallets, ZK dev tooling — and we started expanding builds onto Aleo and Espresso to address them. The ETH Denver 2023 talk remains the canonical record of the era.

1H 2023 — Multi-chain expansion. We shipped private DeFi on Aztec, the Nucleo wallet extension (single-user, multisig, multichain-capable), and private voting plus multiparty-privacy games on Aleo. We ran the 404DAO accelerator with Aleo and Aztec — 200 developers signed up, 50+ made it through the bootcamp, 8 teams formed. Aztec Connect wound down in March; Aztec the company was pivoting to its next-gen chain. Aztec Connect was the L2 our entire B2B product was running on top of, but by then we’d already expanded builds onto Aleo and Espresso, so the sunset accelerated a transition we’d been planning rather than opening a hole.

Puzzle era.

2H 2023 — Rebrand to Puzzle. The accelerator had taught us we couldn’t count on devs alone for first-party experiences — we had to build the consumer-facing products ourselves. We rebranded from Nucleo to Puzzle as the consumer pivot solidified, and shipped the Puzzle extension. The 4 accelerator teams shipped production-quality apps on Aleo using our stack — including arcane.finance, still live today. We struck the Coinbase × Aleo × Puzzle integration deal (going live Q1 2025). At Devconnect we won Aleo’s SnarkTank competition with Where’s Alex — the first publicly-released ZK provable multiparty game, forked 70+ times in the months after.

1H 2024 — First ZK consumer surfaces + road to mainnet. By Q1, 20+ teams were building with Puzzle dev tools and Puzzle Wallet; the ZK Hackathon on top of our stack produced 100+ end-to-end games, with 3 external teams shipping production-quality. In January we launched Puzzle zkGames & Giveaways on Aleo. In February we shipped the first ZK privacy mobile app — Puzzle Wallet on iOS, with Aleo account abstraction. At ETH Denver 2024 we introduced the Puzzle Arcade — ZK-native games, points, and real rewards from real shops. First merchant partners: Krewe, Cajun Power, Motier. The Aleo network ran into real issues on the road to mainnet; we became core protocol contributors out of necessity, not just enthusiasm.

2H 2024 — Aleo mainnet + Puzzle Validator. Aleo mainnet launched on September 18, 2024. The same day, Puzzle Wallet v2.0 shipped — the full Arcade experience unified in the wallet — and Puzzle Arcade went mainnet. Puzzle came out as an Aleo validator securing 20M ALEO — approximately $120M in headline AUM at launch valuation. Within weeks, Puzzle Arcade became the highest-volume zero-knowledge application in the world, after Worldcoin. We shipped Puzzle Pro on mainnet — the user-paid subscription tier covering operating costs so shops can send giveaways directly to verified humans, no ad network in between — plus more Arcade quests, Mystery City, and Squash.

1H 2025 — Coinbase live + 10× scale + proof of human. The Coinbase × Aleo × Puzzle integration went live. Puzzle became part of Coinbase’s Quests surface. (Coinbase has since sunset Quests, but the integration video remains the canonical public record.) The Arcade did a 10× expansion: 10× the shops, 10× the daily giveaways, 600,000 lifetime users. We tightened proof-of-humanhood significantly to solve the KYC fraud problem — earlier Arcade had attracted enough bot behavior that the conservative count after pruning suspicious cohorts is closer to 300,000, which is what we pay rewards against and would defend publicly.

2H 2025 — Growth + Capital. Q3 shipped the referral program, content-creator program, and gift-card uploader rewards — letting brands spin up giveaways in minutes without talking to us. Q4 brought stablecoin integration with Paxos × Aleo on USAD — making instant USD payouts possible — and the expansion of Puzzle Capital, the institutional arm, to 40M ALEO under management.

ZKPuzzle era.

Q1 2026 — The social turn. We added daily puzzle games, private messaging, and group chats. That’s when the product crossed a line most of us hadn’t seen coming when we started: ZKPuzzle wasn’t just a rewards app anymore. It was a consumer social app. Group chats, daily habit, real-world payouts, and a vibe that made people want to show it to their friends — Chipotle gift cards, $180-in-gift-cards-in-a-month stories, a 47-day streak from a user in Austin who’d built her morning around the daily puzzle.

Q2 2026 — the GTM push.

The Q2 2026 push is the most focused growth motion we’ve run. We have a core community of about 6,000 members in Discord who’ve been beta-testing the 3.0 build for over a year, and roughly 1,000 highly active users whose feedback has shaped every release. Starting next week, we’re manually onboarding friends, family, and nearby shops for the final 1% polish. From mid-May onward, we’re opening the TikTok, Instagram, and YouTube Reels push. This is the first time in four years we’ve pointed the distribution engine at normal people in earnest.

On the Business side, we’re going shop-to-shop — literally. If you’re an independent brand looking for a customer-acquisition channel that doesn’t require paying ad networks to reach mostly-bots, email us. On the Capital side, we have an anchor client booked through September and are selectively taking on institutional partners building on non-correlated, ZK-native yield rooted in real-economy flow.

Everything that was true the day Nucleo shipped its first private multisig is still true: fostering next-generation opportunity requires privacy, requires verifiability, and requires that everyone — not just the crypto-native — can come onchain without needing to understand the math underneath. We’ve now done that at a scale most of our early critics didn’t think was possible.

Check out our full research record

The bet.

The four-year track record above is the case for the company. The bet is on what we’re heading toward — the plan, the outcomes if the plan plays out, and the commitment to it.

The master plan.

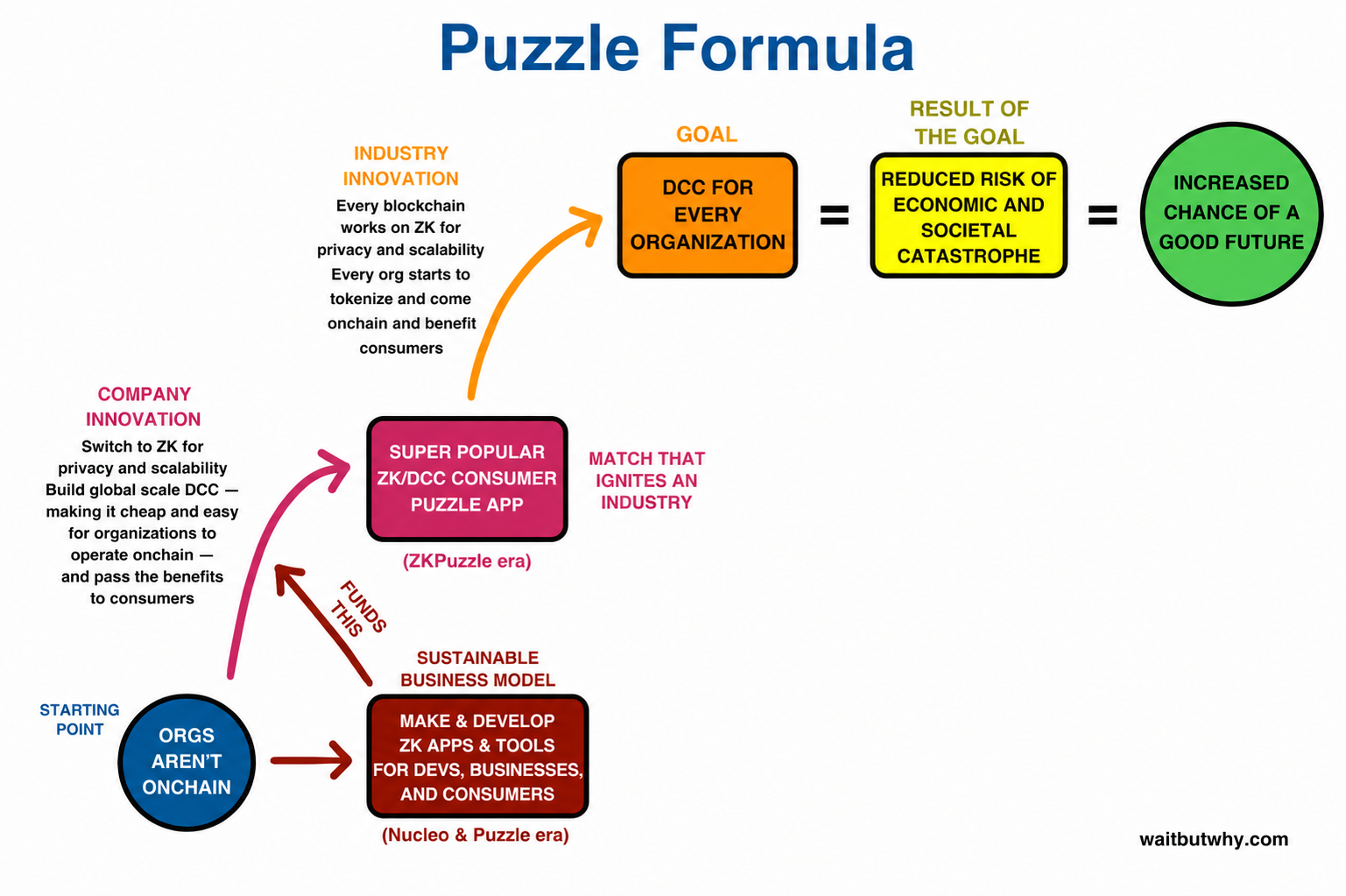

The thesis was something Matt and Luke worked out on a whiteboard in Q4 2022, modeled loosely on the Elon Musk company-strategy diagram Tim Urban laid out on Wait But Why:

What success looks like.

Success means triple-entry extends past the one specific lane it’s lived in for fifty years — to every kind of organization, every category of work, and every part of society.

At industry scale.

Research labs and DOE national labs. The researcher whose commercializable breakthrough gets partnered out to industry holds tokens in the company that productized it — capturing equity her institution’s flat licensing fee never represented.

Professional services. The consultant who builds a new line of business — onboards the early customers, designs the methodology, hires the team — holds a token stake in the line itself, sharing in the revenue instead of watching it accrue to firms and partners who hadn’t built any of it.

Bird and the broader micromobility wave. The squeeze that broke the category was between capital markets demanding faster growth and city governments wanting scooters off the sidewalk. Triple-entry would have changed who was on each side. If city governments and local citizens held tokens in the local Bird rollout, the adversarial dynamic dissolves — Bird isn’t fighting a regulatory war, it’s running a coordinated rollout with the stakeholders who hold its upside.

The MIT cleantech generation (2006–2011). Engineers who poured years into companies that didn’t survive the VC crunch could have held tokens capturing value across the broader sector. MIT’s Energy Initiative documented the structural mismatch; the mismatch would still be true, but the people doing the work wouldn’t have been wiped out alongside the equity.

The current AI displacement. The people whose work trained the models, whose APIs distributed them, and whose jobs are now being compressed by them have no stake in the AI economy itself — only the engineers and investors building it do. Triple-entry closes that gap by giving everyone affected a real ownership claim, not just the cohort with offer letters. This is the application that matters most this decade — the one that motivates everything else.

At town, city, and state scale.

Lafayette post-2010. Shop owners and contractors who lost income could have held tokens representing stakes in the diversification investments that did happen — the healthcare expansion, the infrastructure projects. Capital flight wouldn’t have outpaced human flight as completely. The residents who stayed would have had something to hold onto.

State and city tokens. A state is just a mega-org. State-issued tokens that pay dividends from public-asset performance, or grant voting weight on civic budgets, run on the same mechanics as token-based equity at any other scale. Triple-entry doesn’t care whether the issuer is a Shopify store, a research consortium, or the State of Louisiana itself.

At national scale.

A partial version already exists for the United States: the S&P 500 + 401k. A paycheck flows into a workplace tax-advantaged account. The account holds shares in a basket of US public companies. The holder participates in those companies’ upside without ever having worked at any of them. That is triple-entry at scale — debit (paycheck), credit (employer contribution), token (equity ownership in the basket). Most working Americans are already inside it without thinking about it.

Workers already exercise meaningful choices inside that system — leaving the default fund, self-directing into specific stocks, rolling to an IRA, switching employers. Triple-entry on broader rails extends the same set of choices to a much broader set of organizations than the 500 publicly listed ones.

The honest case.

None of this is a panacea, and we’re not pretending it is. Three predictable objections, addressed honestly.

Most tokens issued under this model will be worthless. Feature, not bug. Same way most stock options at most startups expire underwater. Token value is a fitness function on actual value created, environment, need, and competitive forces. The equity model has always accepted this trade. Triple-entry generalizes it.

Counterparties will sometimes rug. Employers, partners, and networks already do this today. Reputation scoring plus slashing conditions in smart contracts make rugging structurally more expensive than honoring the contract. Doesn’t eliminate bad actors. Raises their cost.

This doesn’t save Lafayette. If a region’s primary industry collapses badly enough, capital and humans will still flee. What triple-entry provides is the shared-incentive mechanism for everyone in the affected economy to try hard to make it work and shift to a new equilibrium together. That’s a meaningfully different starting point from the one Lafayette had.

That’s the bet.

ZKPuzzle is the company we started in 2022 to bring triple-entry bookkeeping to mass consumer scale. Double-entry bookkeeping was invented during the Italian Renaissance — popularized in part by the Medici family and their banking innovations — and became the financial primitive every modern organization runs on. The bet is that triple-entry follows the same trajectory: from a primitive that today works for one specific lane (VC-backed software) to the universal standard tomorrow.

Venture capital is proof the narrow version already works — Dynamic Collective Capitalism is what it produces in that lane. We believe DCC generalizes to every kind of organization and every part of society, and that this generalization meaningfully reduces the risk of economic and societal collapse. That’s the bet we’re making — and why we’re spending our lives on it.